This article provides readers with key knowledge from Module 1 – Quantitative Methods in the CFA Level 1 program.

目录

[LOS 1.a] Interpreting Interest Rates and Their Components

1. Interpreting Interest Rates

An interest rate is the amount a lender charges a borrower for the use of money, expressed as a percentage (%) of the principal.

In finance, interest rates can be interpreted in three main ways:

- Discount Rate:

The rate used by investors to discount future cash flows to their present value. - Opportunity Cost:

The value that investors forgo when choosing one investment over another (e.g., saving or investing in alternative assets). - Required Rate of Return:

The minimum return investors demand to compensate for the risk of an investment.

2. Components of Interest Rates

The required rate of return can be broken down into several components:

Required Rate of Return = Nominal Risk-Free Rate + Default Risk Premium + Liquidity Risk Premium + Maturity Risk Premium

Where:

- Nominal Risk-Free Rate = Real Risk-Free Rate + Expected Inflation

Explanation of Each Component:

- Real Risk-Free Rate:

The return on a risk-free investment in a world with no inflation. - Expected Inflation:

Compensation for the anticipated decline in purchasing power. - Default Risk Premium:

Additional return required to compensate investors for the risk that a borrower may fail to meet obligations. - Liquidity Risk Premium:

Compensation for the risk of not being able to quickly convert an investment into cash without significant loss. - Maturity Risk Premium:

Compensation for the risk associated with longer investment horizons, where interest rate fluctuations can significantly impact asset prices.

Important Note

Government Treasury securities (e.g., T-bills) are typically considered to reflect the nominal risk-free rate, as they already incorporate expected inflation.

[LOS 1.b] Measuring and Interpreting Returns

1. Measuring Return Over a Single Period

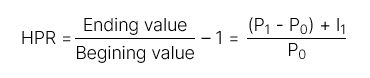

- Holding Period Return (HPR):

The total return earned over a specific holding period.

It includes:

- Capital gains (or losses)

- Income (such as dividends or interest)

2. Measuring Return Over Multiple Periods

| Return Type | Formula | Definition |

| Holding Period Return (HPR) | R = (1 + R1)(1 + R2)…(1 + Rn) – 1 | The return earned over a holding period longer than one year. |

| Arithmetic Mean Return |  | The average return over a given number of periods. It is an unbiased estimate of the expected average return. |

| Geometric Mean Return | ||

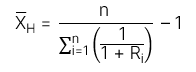

| Harmonic Mean Return | Harmonic mean: Harmonic mean return: Harmonic mean return: | The harmonic mean is a weighted average where weights are inversely proportional to the magnitude of observations. It is commonly used in investment management to calculate the average cost of shares purchased over time. |

[LOS 1.c] Comparing Money-Weighted and Time-Weighted Rates of Return. Evaluating Portfolio Performance

| Money-weighted rate of return – MWR | Time-weighted rate of return – TWR | |

| Definition | MWR is the discount rate that equates the present value of cash inflows with the present value of cash outflows. | TWR is essentially the geometric mean return calculated over the entire investment period. |

| Rule | MWR Calculation Steps Step 1: Identify all cash flows: Cash inflows: All contributions into the account Cash outflows: All withdrawals from the account Step 2: 計算 IRR of these cash flows to determine the MWR. | Step 1: Determine the portfolio value immediately before each cash inflow or outflow. Step 2: Break the total investment period into smaller sub-periods based on cash flow dates. 計算 Holding Period Return (HPR) for each sub-period. Step 3: Compute the overall return by compounding sub-period returns: TWR=(1+HPR1)(1+HPR2)⋯(1+HPRn)−1 注意: If the investment period exceeds one year, use the geometric mean return to annualize TWR. |

In the investment management industry, the Time-Weighted Rate of Return (TWR) is generally preferred because it is not affected by the timing of cash inflows and outflows.

If funds are added to a portfolio during unfavorable periods, the value calculated using the Money-Weighted Rate of Return (MWR) tends to be lower (MWR < TWR). Conversely, if funds are added during favorable periods, the value calculated using MWR tends to be higher (MWR > TWR).

[LOS 1.d] Calculating and Interpreting Other Measures of Return and Their Applications

| Types of Returns | Formula | |

| Gross return and Net return | Gross return | The total return before management fees and expenses. |

| Net return | The total return after deducting management fees and expenses. | |

| Pretax and After-tax Nominal Return | Pretax return | The portion of return before taxes are applied. |

| After-tax return | The portion of return after taxes have been deducted. | |

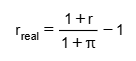

| Real Return and Nominal Return | Nominal Return | 包含: Risk-free rate (Rf) Inflation (π) Risk premium (RP) =>> Nominal return reflects the total return without adjusting for inflation. |

| Real Return |  Real Return Variables: r: Nominal return r_real: Real return π: Inflation rate =>> Real return is the return after adjusting for inflation, representing the true increase in purchasing power. | |

| Leverage Return |  Investors can use leverage by: Borrowing money Using derivatives =>> This amplifies both potential gains and losses. Calculation concept: Profit or loss is measured based on the investor’s actual invested capital (equity), not the total asset value. | |